Table of Content

An insurance company may end up issuing many checks in one claim. By asking questions to your insurance company during the claims process, you can better understand what to expect. It is also helpful to understand what you will need to provide in order to get paid. Disaster claims or major claims may be handled differently from those for a small theft or burglary. Some policies, like high-value home insurance, also offer more flexible payment terms.

One option, if home damage is not too extensive, is to pay for repairs using a home equity loan, rather than making an insurance claim. This can reduce the chance that your homeowners insurance rates could rise as a result of making too many claims. The home insurance claim process can seem overwhelming, but don't worry, we have got you covered.

What is the significance of the claim check being made out to several people?

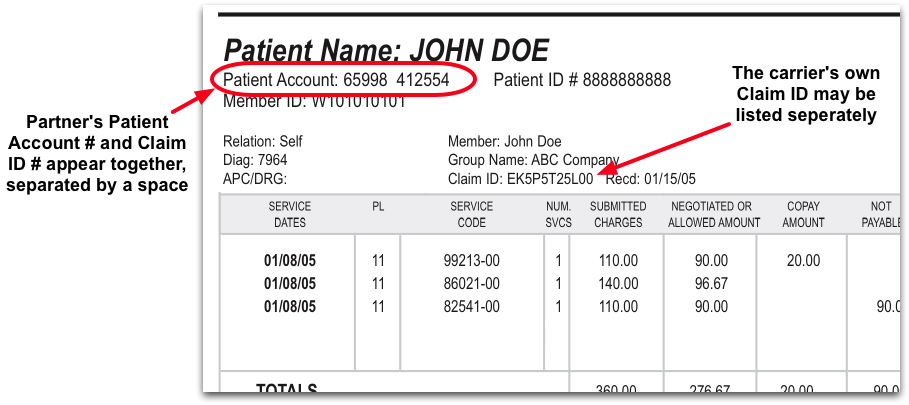

Most relevant to the topic, it will contain details about claims related to the property – including the type of loss of each claim as well as the date and cost of the claim itself. It will even indicate the status of a claim, such as whether or not the claim has been closed, or is pending. Your homeowners insurance policy will not cover some weather-related damages. For example, you need a separate flood insurance policy to cover damage from floods. Some homeowners may also need to purchase a separate wind policy to protect themselves from damage related to hurricanes. You also may need an endorsement on your policy to cover damages from weather events.

Perhaps you want to check for fraud, or want to get an understanding of why your premiums are what they are. Luckily, checking your home insurance claim history can be quite straightforward. Your insurance company will ask you to document the damage if it is safe to do so and may also schedule a time for a claims adjuster to inspect the damage. This is why it is very important to always have a completed home inventory checklist updated and safely saved on a computer, iPhone or app. Home insurance companies may also ask for make, model, serial numbers and proof of photos for ownership.

When not to file a homeowners insurance claim

For starters, call your insurance company as soon as possible after the event to explain what happened. Also, make sure to take pictures and do any necessary repairs to prevent further damage. At Insure.com, we are committed to providing honest and reliable information so that you can make the best financial decisions for you and your family.

To do that you need to learn how to read a homeowners declaration page. The homeowners declaration page is a summary of your insurance policy. It includes a breakdown of what is covered by your policy, so you will want to be familiar with this document. Before the next incident damages your home, you will want to know you have the best rates on home insurance. Enter your ZIP code here for a free comparison of the best homeowners insurance rates in your area. Your check for additional living expenses has nothing to do with repairs to your home.

Search Anything Homeowners!

Most usually go in for third-party insurance because its premiums are the lowest. This policy is also widely opted for due to the lack of awareness about other insurance policies, and how they can protect you in a wider variety of circumstances. Make a mortgage payment, get info on your escrow, submit an insurance claim, request a payoff quote or sign in to your account. Go to Chase home equity services to manage your home equity account. Our affordable lending options, including FHA loans and VA loans, help make homeownership possible.

We've looked at all the homeowners insurance claim check questions you are likely to have, and we have the answers. You'll have to submit a list of your damaged belongings to your insurance company . It is to match the remaining claim payment to the exact replacement cost. If you decide not to replace an item, you’ll be paid the actual cash value amount for it. In some cases, an insurance company may issue multiple checks in response to a single claim.

You may need to hire an attorney if you still don’t understand why your claim was denied after speaking with a representative. An attorney who specializes in insurance claims can help you navigate the appeals process and potentially get your claim paid. Homeowners insurance protects you from financial loss in the event of damage to your home or possessions. However, filing a claim can be lengthy and complicated, and it’s important to ensure that you have a valid claim before proceeding.

A claims adjuster may need to visit your home to inspect the damage. You may complete a "proof of loss" form at this time, which is a formal statement about the loss. Your insurer will either approve or deny your claim based on the adjuster’s evaluation and your documentation. Keep in mind that you might need to send additional evidence if your insurer denies your claim. You can also hire a public adjuster or an insurance attorney to help prove the legitimacy of your claim. Comprehensive insurance policies are definitely a step up from third-party insurance, but it still does not cover everything.

A homeowners insurance claim starts the process of getting you reimbursed if your home or property is damaged. When you receive your insurance check, you'll notice that Wells Fargo is named on it. As the mortgage provider, we have a financial interest in ensuring your property is restored.

See our current mortgage rates, low down payment options, and jumbo mortgage loans. Unfortunately for some homeowners, your mortgage company can hold your check. If a borrower listed as a payee can’t sign the insurance check, call us for information about the documentation we’ll need to proceed. It is also a good idea to have a contractor on site when the claims adjuster arrives. They will know if the adjuster is making an accurate assessment of the repair costs. Next, you will need to contact your provider to let them know you need to file a claim.

One way to get started is by getting the best deal on home insurance premiums. If you are interested in a more affordable home insurance policy, enter your ZIP code to compare rates now. There is no shortage of reasons why one would want to check their home insurance claims history. It is essential for investigating any changes that your insurance may make to their premiums. In fact, claims history is often a significant factor when your insurance is trying to determine premiums, though it isn’t always the main factor.

GEICO has no control over their privacy practices and assumes no responsibility in connection with your use of their website. Any information that you provide directly to them is subject to the privacy policy posted on their website. Manage your American Modern Insurance Group® policy online or speak to an agent for Assurant or American Modern Insurance Group®. Chase's website and/or mobile terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its terms, privacy and security policies to see how they apply to you. Chase isn’t responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the Chase name.

Here are examples to help you understand what to expect for your claims payments. Mila Araujo is a certified personal lines insurance broker with more than 20 years of experience in the insurance industry. As an insurance expert, has written about homeowners, auto, health, and life insurance for The Balance. Mila received the Bernard J. Finestone Award in General Insurance from McGill University in 2001. Staying on top of what the insurance company needs to issue your payment is the best method to collect your total payout for your claim as quickly as possible.

No comments:

Post a Comment